Asset-based lending that scales with you

When your business outgrows invoice-by-invoice funding, it's time for a bigger line. Access more working capital from the assets you’ve built, and keep growing on your own terms.

What is asset-based lending (ABL)?

Asset-based lending is a type of business loan secured by the total collateral on your balance sheet. This includes:

- Accounts receivable (AR)

- Inventory

- Equipment

- Machinery

- Real estate

In one flexible revolving line of credit, you access more cost-effective funding while keeping control of your customer relationships.

Borrow against your total assets

Stay close to your customers

Grow your book, grow your line

.png)

How ABL turns your balance sheet into working capital

Step 1: We size up your assets

We take a close look at your receivables, inventory, and equipment to build your borrowing base: the pool of eligible collateral your line is built on. This step includes a field exam and, where needed, a collateral appraisal, so we can set the right advance rates for your business.

Step 2: Draw what you need, when you need it

Your line works like a revolving facility: draw against your borrowing base whenever you need capital, and only pay for what you use*. As your customers pay down their invoices, your available line refreshes. Meet payroll, win the contract, and plan for your next opportunity.

*Unused line fees and annual fees will apply.

Step 3: You grow, the line keeps up

Your borrowing capacity grows with your book. Take on a new customer or enter a new market without having to refinance from scratch. Eligible line increases come with minimal paperwork, so you can stay focused on the business.

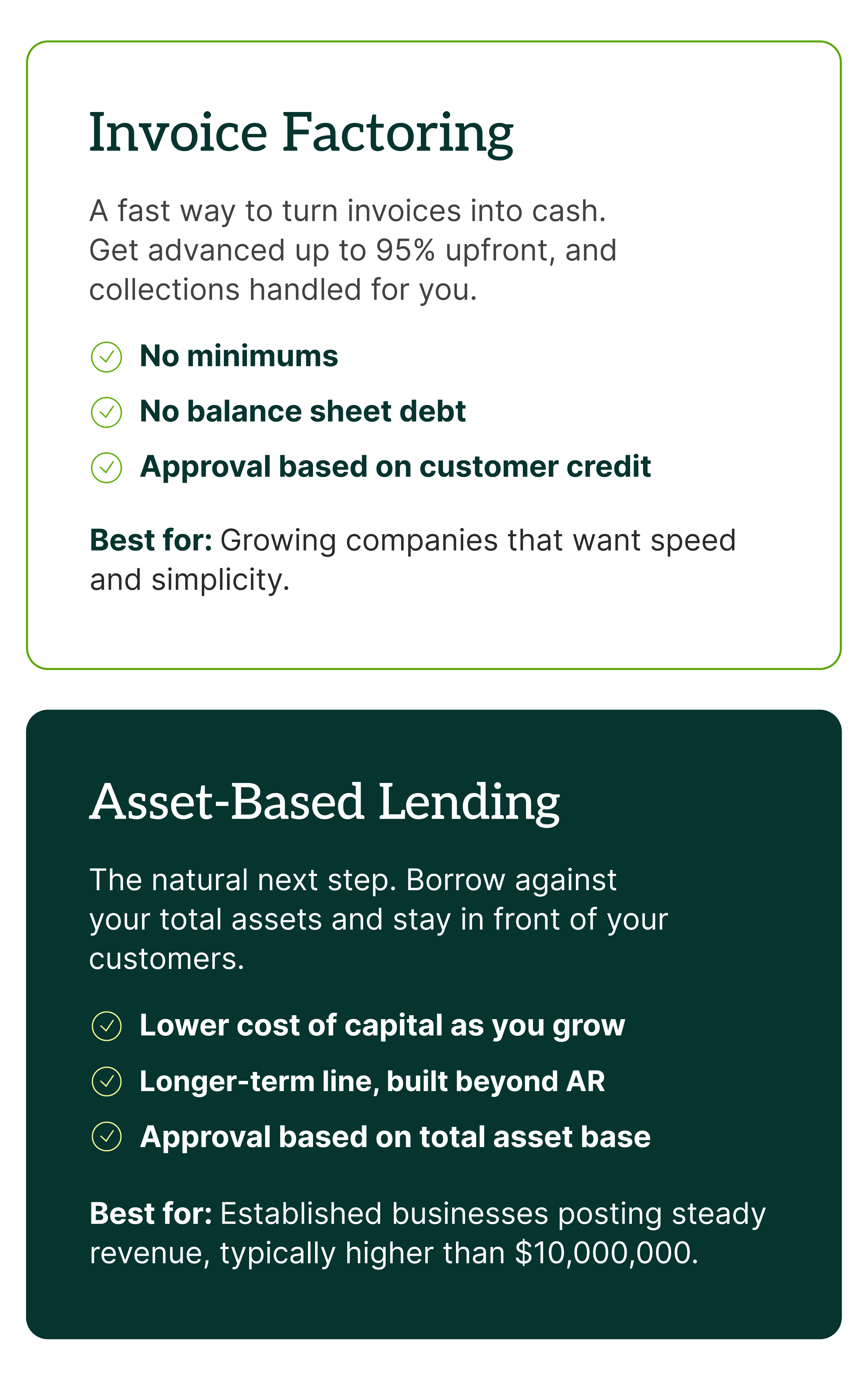

Invoice factoring or asset-based lending: which is right for your business?

Success stories to inspire your business

Discover how we help businesses like yours transform challenges into triumphs.

.jpg)

Like many others in the industry, A.B. Staffing was looking to expand their operations after another challenging year in the staffing sector. Confronted with the need for capital to expand, A.B. Staffing faced a common hurdle securing funds quickly without the complex, equity-diluting process that’s typical of raising capital. Their goal was clear – to find a way to scale efficiently without relinquishing ownership.

Choosing an alternative path, they partnered with Meritus Capital for financial support. This partnership offered a much-needed advantage with immediate access to the capital they required, sidestepping the pitfalls of equity dilution.

With the resources to move forward, A.B. Staffing leveraged this opportunity to broaden their operations and tackle new opportunities, all without sacrificing ownership control of their business.

Meritus Capital's tailored financial solutions empowered the staffing company, providing hassle-free, flexible, and immediate access to funding. Today, A.B. Staffing has expanded beyond their initial goals and continues to be a major leader in the staffing industry.

.jpg)

Having experienced a nearly $36MM dollar increase in annual sales, this staffing logistics company was hit hard with growing pains. Sales increases are exciting – but when combined with a shortage of resources, they can create serious operational hurdles. To make matters worse, this company’s previous factor was no longer willing to work with them due to their rapid growth pace.

This company needed a solution that would give them:

- A high advance rate of over 93%

- A low factoring fee

- Staffing industry expertise to support their scaling efforts

Meritus Capital saw this company’s setback as an opportunity. After taking them on as a new client, the Meritus team delivered quickly on all fronts:

- A rate that met their growth needs

- 25% savings on their factoring rate

- A partnership driven by an industry-specific growth strategy

The result?

The client was well-positioned to jump on the exciting opportunities coming their way. Most importantly, they gained a financial partner who set them up for long-term profitability, and plenty of room to keep growing.

Staffing is a highly competitive industry that thrives on service excellence – and working with a likeminded factor makes all the difference. Meritus is here to support your business with the tools and flexibility to face rapid growth with confidence.

.jpg)

Meritus Capital had a well-established direct hire client who was hungry for an expansion into the temporary staffing market. It was the right move for their business, but it came with time and cash flow challenges.

Payday doesn’t ‘wait.’

Our client was responsible for covering their temporary workers’ payroll expenses. This means they couldn’t risk waiting on employers to pay their invoices, and that extra cash flow was needed to keep the business running as smoothly as possible.

Our client also needed to seize growth opportunities coming from a new market. With growth opportunities, comes greater overhead. Think: extra costs for recruitment advertising, interviewing, background checks, and all the administrative work in between.

Eager to help, the Meritus Team got to work on a new payroll funding line for our client.

The result?

A financing plan that fueled the company’s expansion by 13 times in their new temporary staffing division.

With the right financing partner, you can tap into new markets with confidence. In this case, Meritus Capital was instrumental in broadening our client’s range of staffing needs and revenue streams.

The staffing industry stands as one of the most competitive. Whether you’re starting from scratch or expanding your offerings to gain an edge, Meritus Capital is here to support you in navigating challenges, capitalizing on market trends, and driving sustainable growth so your business can make its mark.

.jpg)

This successful staffing company generating $30MM annually was facing a significant challenge: high financing fees from their previous funder were severely limiting their growth potential.

When fees are excessively high, they can create substantial obstacles for businesses. These fees drain valuable capital that could otherwise be reinvested into essential areas like expansion, hiring, or new projects. As a result, companies often find themselves:

- Trapped in a cycle of debt, constantly playing catch-up, and shrinking profit margins.

- Unable to seize new opportunities or improve operational flow, creating roadblocks to growth.

Here’s how Meritus turned things around for them:

- Introduced a competitive and cost-effective financing solution: We customized our approach to meet the staffing company’s specific needs, easing their financial strain.

- Saved over $100,000 in financing costs within 12 months: A significant reduction in fees freed up hard-earned capital that had previously been tied up.

- Empowered the company to reinvest in growth initiatives: With the financial relief, they could focus on expanding operations and pursuing new opportunities.

By customizing our solution, we alleviated the burden of high fees, giving the company the financial space to concentrate on what really matters: growth and longevity.

Every day, our team is excited to help businesses overcome challenges and achieve new milestones. By understanding each client's unique needs and addressing the core issues, we’re proud to have helped hundreds of businesses reach their fullest potential.

Frequently asked questions

You continue managing your customer relationships. To keep your line current, customer payments are directed to an account designated by your lender to pay down your balance. You draw back against your available line as you need it. It's a standard part of how asset-based facilities work, and it keeps your borrowing base and availability in sync.

Absolutely. That's exactly how we like to work. Many businesses start with factoring or payroll funding and move to an asset-based line as their revenue and balance sheet grow. Because we offer the full range, the transition is seamless, and you keep the same team that already knows your business.

Not like a traditional bank loan. We require a Fixed Charge Coverage Ratio (FCCR), or minimum Tangible Net Worth (TNW). We shape any covenants around your business, and strong borrowers often carry very few, if any.

Asset-based lending involves a bit more due diligence than factoring. Typically, ABL includes a pre-funding field exam and, in some cases, a third-party collateral appraisal. Once your facility is in place, you'll provide regular borrowing base reporting, typically weekly, so your available line stays current as your assets change. Our team guides you through every step.

Most commonly your accounts receivable, which carry the highest advance rates. Depending on your business, your borrowing base can also include inventory, machinery, equipment, and real estate. We'll help you identify which of your assets qualify and what they can unlock.

Asset-based lending (ABL) is designed for businesses with strong, steady revenue and solid financial reporting. If you've outgrown straight factoring and you're looking for a larger and more cost-efficient line, it's worth a conversation. Not quite there yet? Our invoice factoring and payroll funding solutions are a great place to start, and we'll help you graduate to ABL when the time is right.

With invoice factoring, also known as payroll funding in the staffing industry, you sell your receivables, we advance the cash, and then we collect payment directly from your customers. With asset-based lending, you keep your receivables and borrow against them (along with your inventory, equipment, and other eligible collateral) through a revolving line of credit without handing your accounts to a third party. Factoring is built for speed and flexibility, and ABL is built for established businesses that want a larger, lower-cost line and more control.

There are many reasons why a business would want to utilize invoice factoring such as: rapid growth, long drawn out payment terms from their customers, and demanding payroll.

The two main pieces of criteria you should think about before applying for invoice factoring are: Is the work you are invoicing for complete? Are my clients credit-worthy (if you're not sure, we can check for you!) Beyond that, there is a short application process so we can understand your business.

A lot of it comes down to you and how quickly you can get us the documentation we need. For invoice factoring, businesses can typically expect 7–14 days, but with our online application and easy eSigning, the process is faster than ever. With Meritus Capital, first funding can happen in as little as 3–7 days if everything goes smoothly.

An asset-based line of credit takes a little longer to set up. By nature, ABL involves more moving parts, so there's additional due diligence up front, including a field exam and, where applicable, a collateral appraisal. That extra step is what allows us to build a larger, more flexible line around the full value of your assets, so it's time well spent for businesses ready for it.

Factoring companies do need a 1st position UCC filing on the accounts receivable of the business they are providing factoring for. That being said, there are many cases where agreements can be made between lenders to facilitate factoring even if you have some other type of financing. Speak with someone at Meritus Capital to discuss your situation and how we may work together.

More questions? We're here to help.

Send us a note and our team will reach out to you or simply call us at 877-648-3709